Panama is facing a US$140 million international arbitration claim over an energy project that never generated a single megawatt of electricity.

The dispute, filed before the International Centre for Settlement of Investment Disputes (ICSID), has drawn renewed attention to a broader question facing governments across emerging markets: how should regulators balance investor protection with accountability when large-scale projects fail to materialize?

In Panama’s case, the controversy traces back to two ambitious developments linked to businessman Kenneth Zhang—a port project and an LNG-to-power venture. Both were promoted as strategic investments. Neither was completed. One has now become the basis of a major international claim against the Panamanian state.

The case raises questions that extend well beyond a single arbitration. It touches on regulatory oversight, concession management, and the challenges governments face when investment commitments remain unfulfilled for years while licenses and concessions continue to remain in force.

Two Projects, One Common Thread

Kenneth Zhang’s name appears in connection with two separate projects that, despite operating in different sectors, followed remarkably similar trajectories.

The first was a port development on Isla Margarita, near the Atlantic entrance to the Panama Canal. The second was a large-scale liquefied natural gas (LNG) project in Puerto Pilón, Colón, designed to expand Panama’s power generation capacity.

Both initiatives were presented as transformative investments with the potential to contribute significantly to the country’s economic development.

Neither ultimately materialized.

The Isla Margarita Port Development

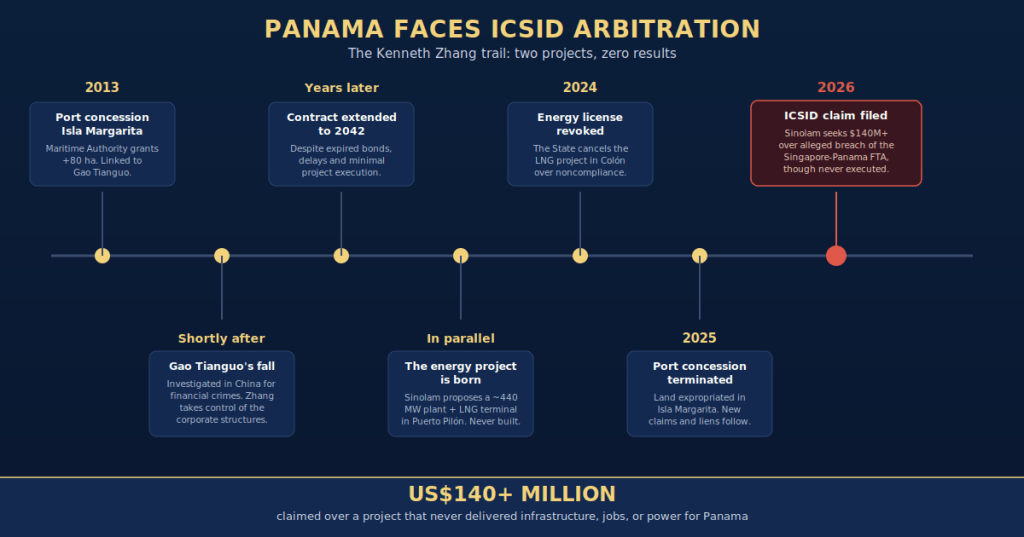

The port project dates back to 2013, when the Panama Maritime Authority granted concessions for the development of a cargo terminal and container yard covering more than 80 hectares of seabed in a strategically important maritime zone.

At the time, the project was associated with Chinese businessman Gao Tianguo, also known as Ko Tin Kwok, who would later become the subject of financial crime investigations in China. Following his departure from the venture, Kenneth Zhang emerged as a key figure within the corporate structures controlling the concession.

The project envisioned investments valued in the hundreds of millions of dollars. Yet despite those commitments, development activity remained limited. Audits and official reviews documented prolonged inactivity, delays in contractual obligations, expired performance bonds, and a series of compliance deficiencies.

Nevertheless, the concession remained active for years and was eventually extended through amendments until 2042.

As the project stalled, disputes among investors and shareholders surfaced. Litigation filed in the United States alleges that Zhang consolidated control of the venture through a combination of share transfers, management changes, and corporate restructurings that displaced other investors. According to the complaint, assets associated with the project ultimately changed hands under conditions that did not reflect their full market value.

Over time, the concession became associated less with infrastructure development and more with extensions, restructurings, and unresolved disputes.

The situation culminated in 2025, when the Panamanian government terminated the concession following years of noncompliance and ordered the expropriation of lands linked to the project. The decision triggered a new wave of litigation, competing claims, and asset disputes among stakeholders.

The port project had come to an end.

The Energy Project That Never Reached Construction

At the same time, a second initiative linked to the same corporate network was being promoted in Colón.

Through Sinolam, developers proposed an integrated LNG-to-power project consisting of a combined-cycle power plant with an expected capacity of approximately 440 megawatts, an LNG receiving terminal, and supporting storage infrastructure designed to secure fuel supply.

On paper, the project ranked among the most ambitious energy investments proposed in Panama in recent years.

In practice, it never advanced beyond the planning stage.

Despite years of promotion, none of the project’s core components were ever built. The proposed power plant, LNG terminal, and storage facilities remained unconstructed throughout the life of the concession.

As a result, the project generated no electricity, created no employment, produced no infrastructure, and delivered none of the economic benefits cited in support of its approval.

Yet for years it remained classified as a strategic investment.

The implications extended beyond the project itself. Regulatory resources, market expectations, and long-term planning assumptions remained tied to an initiative that never reached execution. During that period, alternative market participants and competing solutions operated within an environment shaped by a project that continued to exist administratively despite the absence of tangible progress.

The license was ultimately revoked in 2024.

From Unbuilt Project to International Claim

The dispute did not end with the revocation of the license.

Sinolam International subsequently filed an arbitration claim before ICSID seeking more than US$140 million in damages. The company argues that Panama violated protections contained in the Singapore–Panama Free Trade Agreement by revoking the concession without adequate notice and without providing sufficient due process guarantees.

The claim presents a striking contrast.

The underlying project never entered construction, never generated power, never created jobs, and never delivered infrastructure. Nevertheless, it is now being presented as an investment that suffered losses warranting substantial compensation.

This tension lies at the heart of the dispute.

While governments grant strategic licenses with the expectation that projects will ultimately produce public and economic benefits, investment arbitration frameworks may also recognize investor expectations and treaty protections independent of a project’s operational status.

The legal merits of the case will ultimately be determined through arbitration. The broader policy questions, however, remain.

How should governments assess the value of projects that never advance beyond the planning phase?

At what point should prolonged nonperformance trigger regulatory intervention?

And how can regulators protect both legitimate investors and the public interest when major projects remain dormant for years?

The Cost of Delay

One of the most significant aspects of the case may be the opportunity cost associated with prolonged inactivity.

Large infrastructure and energy projects do not operate in isolation. They influence planning decisions, market expectations, regulatory priorities, and investment strategies. When projects remain active despite failing to achieve key milestones, they can affect the timing and development of competing alternatives.

In the energy sector, such delays can have consequences that extend beyond project sponsors. Prolonged uncertainty may affect capacity planning, market competition, and the introduction of new generation resources capable of strengthening the electricity system.

From that perspective, the costs associated with nonperformance are not necessarily borne exclusively by investors.

They may also be absorbed, directly or indirectly, by consumers, businesses, and the broader economy.

This creates a difficult paradox.

A project that never generated electricity, never created the promised jobs, and never delivered the anticipated economic benefits is now seeking a nine-figure compensation award, while the country itself absorbed years of uncertainty associated with its delay and eventual failure to materialize.

Beyond the Arbitration

The significance of this case extends beyond the outcome of a single arbitration proceeding.

It highlights the importance of ensuring that concession frameworks include effective mechanisms to distinguish viable projects from proposals that remain indefinitely in the development stage. It also underscores the need for clear accountability standards when strategic investments fail to meet the milestones that justified their approval.

Panama, like many emerging economies, depends on foreign investment to support growth and development. Maintaining legal certainty and honoring legitimate investor protections are therefore essential.

But legal certainty must serve a broader purpose than protecting investment alone.

It must also safeguard the public interest, preserve market integrity, encourage fair competition, and ensure that strategic concessions ultimately deliver the economic and social benefits they promise.

The arbitration involving Sinolam and the projects associated with Kenneth Zhang may ultimately be decided by legal arguments and treaty interpretation.

The larger lesson, however, is one of governance: ensuring that ambitious investment announcements are matched by execution, accountability, and results.